MARKET NOTES MAY 2026 PWJohnson Wealth & Legacy

Crude is above $100, inflation is sticky, and central banks are tightening again — yet equities keep printing records. That looks like complacency. The numbers say otherwise.

~7 min read

The headlines read like a recipe for a sell-off. Conflict in the Middle East has pushed crude past $100 a barrel, reignited inflation, dented growth, and nudged central banks back toward tightening just as the cycle seemed to be steadying. Equities paused for a few sessions — and then went right back to doing what they have done for months: setting records. The obvious question is whether investors have simply stopped paying attention.

I don’t think they have. When you set the headlines aside and look at the three forces that actually move markets over time — earnings, valuations, and flows — a calmer picture comes into focus. The rally isn’t built on wishful thinking. It’s built on arithmetic.

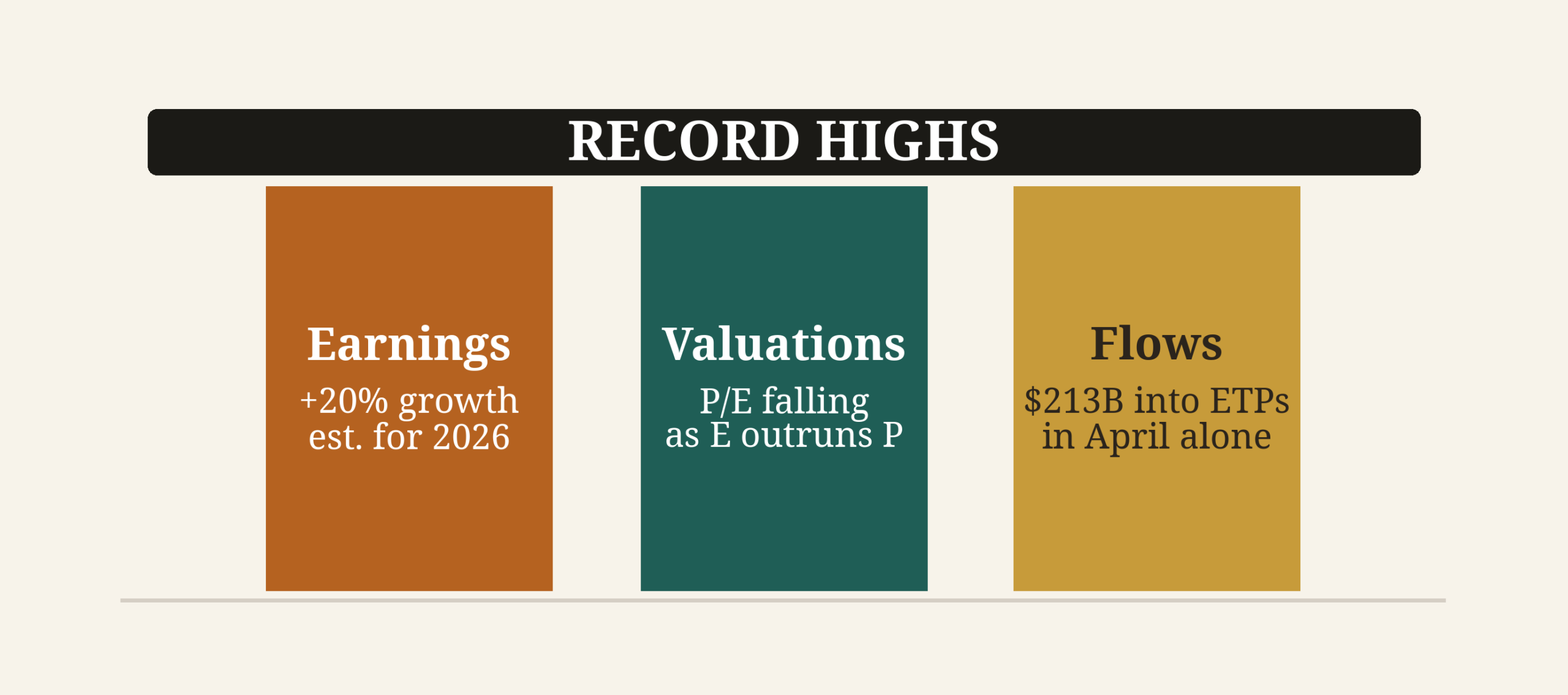

THE ARGUMENT, AT A GLANCE

Three pillars holding up record highs

The case for a rational market rests on three measurable supports rather than on sentiment.

REASON 01

Earnings are doing the heavy lifting

Over any meaningful horizon, profits are what markets track — and right now profits are surprising to the upside.

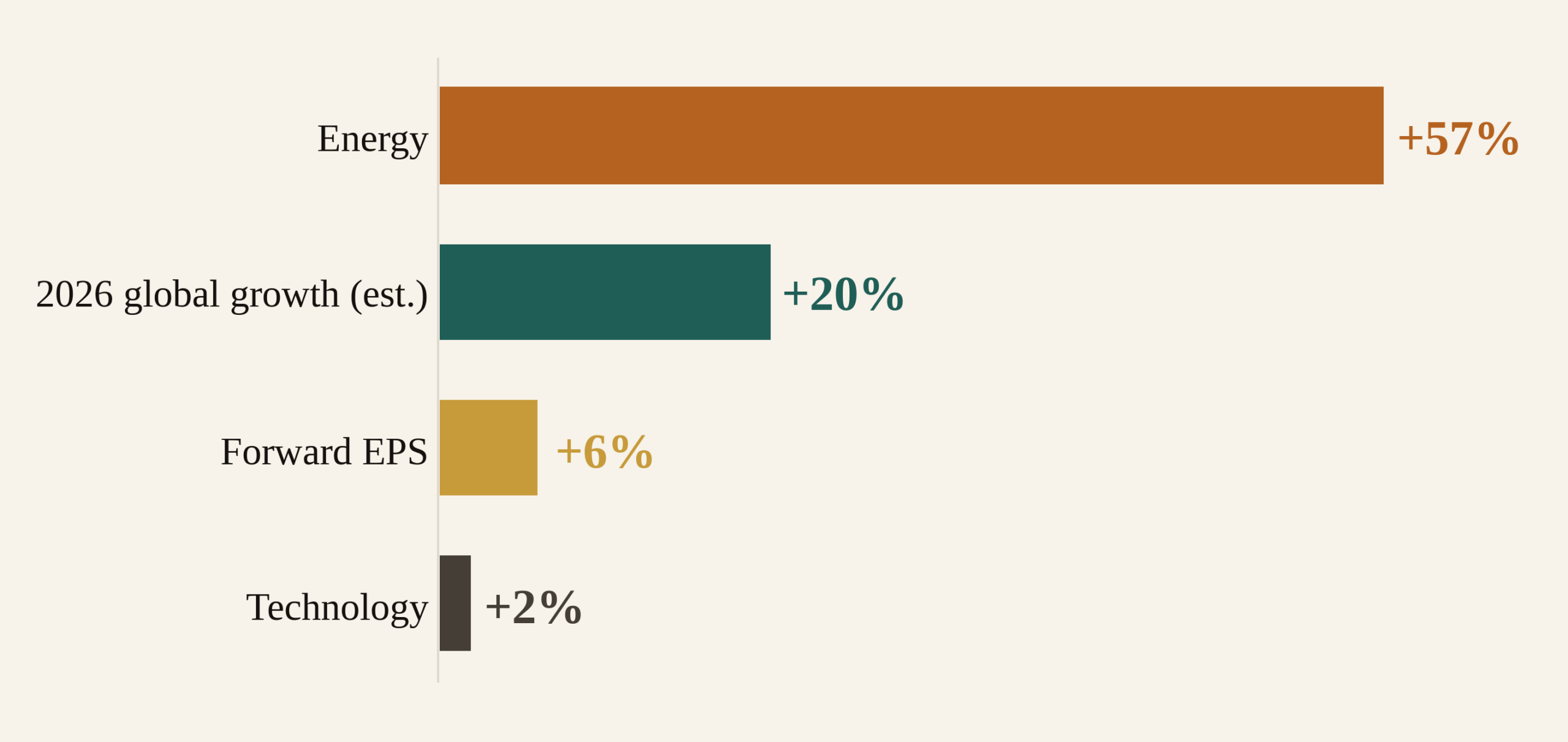

Analysts now expect roughly 20% global earnings growth in 2026, and forward earnings-per-share estimates have been revised up by more than 6% since the late-February escalation, according to Goldman Sachs. That is the opposite of what a conflict-driven growth scare is supposed to produce.

Energy did much of the heavy lifting, with earnings expectations jumping about 57% as oil climbed. But the strength was broad. Even technology — a sector that entered the year with already-rich forecasts — picked up a further 2% upgrade. When the most expensive corner of the market is still getting earnings upgrades during a geopolitical shock, that tells you something about the underlying engine.

EARNINGS REVISIONS SINCE LATE FEBRUARY

Upgrades, not downgrades — led by energy

Revision magnitudes per Goldman Sachs; 2026 global growth shown as the consensus expectation rather than a revision.

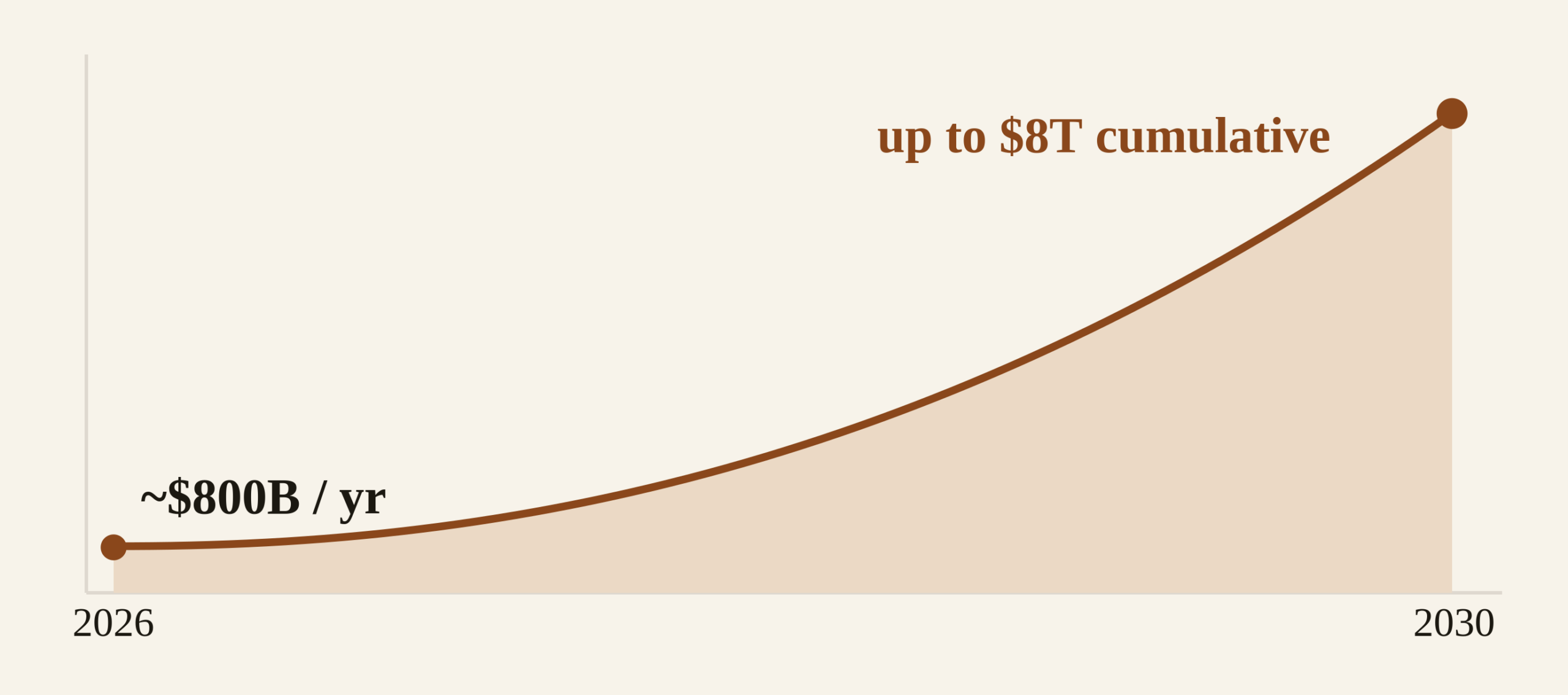

The engine, of course, is artificial intelligence. Capital spending on AI is running toward roughly $800 billion in 2026, and BlackRock Fundamental Equities estimates the cumulative build could reach as much as $8 trillion by 2030. For the companies supplying the memory, the chips, and the power behind that build-out — concentrated in the U.S. and Asia — this is less a one-year story than a multi-year source of earnings support.

THE CAPITAL BEHIND THE RALLY

AI investment: from ~$800B a year to a possible $8T build

Annual 2026 spend per industry estimates; cumulative 2030 figure per BlackRock Fundamental Equities. Curve illustrates trajectory, not a precise path.

There’s a second-order effect worth noting. AI is extraordinarily energy-hungry, and that appetite lands on top of an existing energy shock. Together they are likely to accelerate an “all of the above” approach to power — fossil fuels and renewables alike — as governments lean harder into energy independence. For stock pickers, that points to real growth in energy infrastructure, clean generation, transmission, and efficiency.

REASON 02

Valuations are cooler than the indices suggest

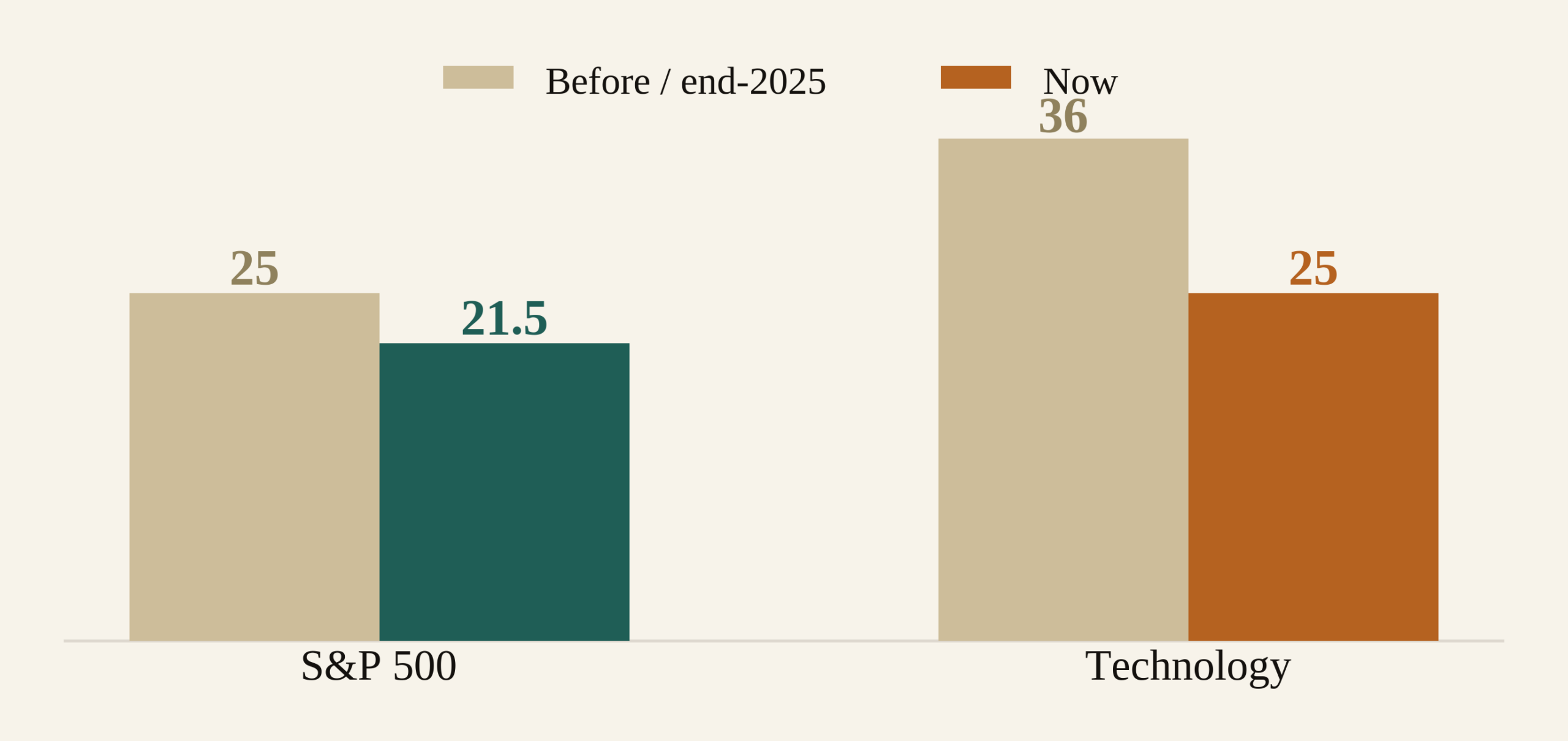

Here is the counterintuitive part: prices are near records, but multiples have actually come down.

Because earnings have climbed so quickly, price-to-earnings ratios look less stretched than they did a few months ago, not more. The S&P 500’s P/E has eased to around 21.5, down from above 25 before the conflict, on Goldman Sachs figures. The move is even sharper in technology, where the multiple sits near 25, down from 36 at the end of 2025, according to LSEG.

PRICE-TO-EARNINGS, BEFORE VS. NOW

Multiples compressed as the “E” outran the “P”

S&P 500 multiples per Goldman Sachs; technology multiples per LSEG.

When the price line lags the earnings line, “record high” and “expensive” stop being the same sentence.

This is why fears of rampant complacency may be overdone. If the conflict finds a durable resolution — and the Strait of Hormuz reopens — the next leg higher need not depend on a handful of AI names. Leadership could broaden out.

REASON 03

The money keeps showing up

Strong profits and reasonable prices have kept investors leaning into risk.

Flows confirm the stance. BlackRock data shows $213 billion moving into global exchange-traded products in April — the sixth-largest monthly inflow on record. The bulk of it, around $150 billion, went into equities, and commodity funds drew positive flows too. Given how solid the fundamentals of today’s market leaders look, that’s a trend more likely to continue than to snap.

APRIL FLOWS INTO GLOBAL ETPS

$213B in, with equities taking the lion’s share

Per BlackRock; April ranked the sixth-highest month for global ETP inflows on record.

THE RISKS

Clouds on the horizon

None of this means the coast is clear. Two risks deserve a clear-eyed look.

Sticky oil. If crude stays elevated through 2026, the knock-on effects — shortages of refined products, higher inflation, slower growth — could intensify. Valuations have adjusted somewhat to reflect that uncertainty, which is part of why prices haven’t fully kept pace with earnings. But it’s hard to argue markets have fully priced the risk, especially given the scale of the supply shock and the pressure building in the bond market.

An AI pullback. The other risk runs through the rally’s own engine. If the largest AI spenders trim their plans — under shareholder pressure, or because the consumer weakens — just as a wave of new semiconductor capacity comes online, the supply-demand imbalance that currently favors chipmakers and the broader AI chain could flip uncomfortably fast.

| THE BOTTOM LINE Questions about complacency in the face of geopolitical and macro uncertainty are entirely legitimate. But judged by the three metrics that usually matter most — earnings, valuations, and flows — this market doesn’t look frothy. It looks decidedly rational. |

SOURCES — Goldman Sachs (earnings revisions, S&P 500 P/E); BlackRock Fundamental Equities (AI capex, ETP flows); LSEG (technology P/E). Analysis adapted from Reuters market commentary, May 2026.

This material is for general informational and educational purposes only and reflects a point-in-time market commentary. It is not investment, tax, or legal advice and is not a recommendation to buy or sell any security. Forecasts and estimates are inherently uncertain and may not come to pass. Consult a qualified professional before making financial decisions.